By Jeff Megayo*

In 1953, the State of Kuwait established the world’s first Sovereign Wealth Fund (SWF) to manage the surpluses of its oil revenues. Since then, particularly during the past twenty years, there has been a proliferation of SWFs globally as countries have discovered enormous natural resources and gained significant revenues from them. There are presently over 20 SWFs in Africa, and many other countries such as South Africa and Kenya are creating their own. The performance of most of these organizations is difficult to gauge because of their opacity. Nonetheless, there are existing SWFs that African countries can study to carry their mandates.

One such organization is the Government Pension Fund Global of Norway (the Fund). The Fund is the largest SWF globally by Assets Under Management (AUM) and of the most transparent. Interestingly, although Norway is a wealthy oil nation, many countries earn far more from natural resources. Therefore, the country’s SWF size results from many other reasons than the oil revenues that the government makes. It is, consequently, worthwhile for African policymakers to critically analyze Norway’s Fund to improve their SWFs to achieve the mandate for which they were established.

Overview of Norway’s Sovereign Wealth Fund

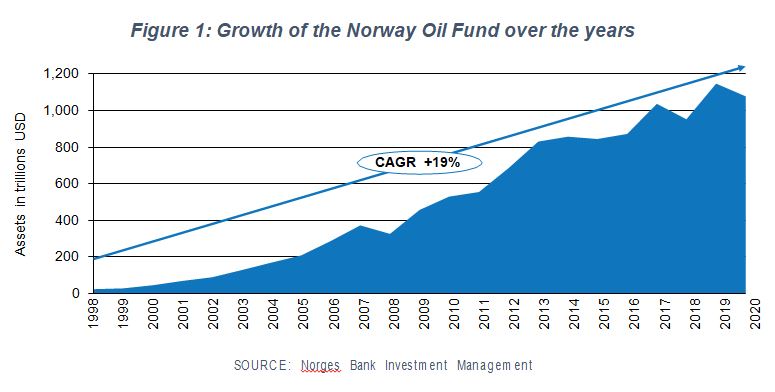

For 30 years, the Government of Norway has saved lots of money for its citizens through its sovereign wealth fund. The Government has amassed an asset of over USD 1 trillion for its population of just 5.33 million people. That puts Norwegian citizens among the wealthiest on earth based on the Fund’s holdings alone. During most years, the returns have been phenomenal. In 2017 alone, the Fund returned USD 131 billion. If this benefit were an African country, it would represent the 5th largest economy in the continent.

How did Norway manage to establish one of the largest corporations in the world, with an exemplary governance structure?

The Beginning

Oil Discovery

Norway was a latecomer to the oil industry. The country only began oil drilling in 1966, well after most oil-producing nations such as the United States, Saudi Arabia, and Nigeria. Nonetheless, the growth of Norway’s oil industry surpassed anyone’s expectations.

In 1969, Phillips Petroleum made a significant discovery off the North Sea: the Ekofisk oil field. But commercial production only started in 1971. The Ekofisk oil field remains one of the most important offshore oil fields ever discovered in the world. At its peak in late 1976, the Ekofisk oil field alone produced over 350,000 barrels per day.

Subsequently, oil companies made world-class discoveries soon after Ekofisk. The Norwegian Government doubled down on the sector through policies and investments. In 1972, Statoil, the state petroleum company, was created to enable Norway to be an active player in the oil industry and “build up Norwegian competency within the petroleum industry.”

Oil demand grew exponentially, and the Fund benefited from increased oil prices, particularly from 1973 until the mid-80s and again from the general rally of oil prices from 1999 until 2008. This sequence of events, coupled with the Norwegian Government’s informed decision-making, caused a boom in Norway’s economy.

The government knew the euphoria wouldn’t last

Although the oil industry boom fueled Norway’s economic growth, the country witnessed swings in oil prices. Its leaders were also aware that oil revenues would eventually drop. By the early 1980s, formal discussions began on Norway’s oil industry’s role in its economy. Experts recommended establishing a SWF to manage oil revenues in the interest of the long-term growth of the economy and the Norwegian people.

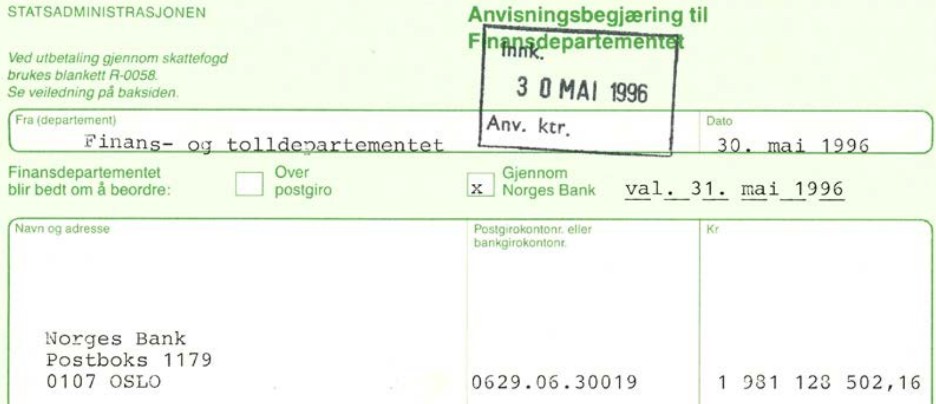

In 1990, Norway’s Parliament legally established the Government Petroleum Fund. The first capital transfer occurred six years later from the Ministry of Finance to the Fund. It was a total sum of NOK 1,981,128,503, the equivalent of approximately USD 310 million. Twenty-four years later, the Fund had a market value of USD 1.1 trillion.

Figure 2: The first capital transfer in the amount of NOK 1.981 billion to the Oil Fund occurred on 30 May, 1996

SOURCE: Norges Bank

Lessons for Africa’s Sovereign Wealth Funds

The incredible success of Norway’s SWF left clues, which African countries could study in building a sustainable future for their people. Resource-dependent African countries do not need to reinvent the wheel. Developed countries like Norway also merely adopted policies and strategies that worked elsewhere. Therefore, African countries should leverage the following best practices established by Norway to elaborate or enhance their SWFs’ performance. However, each government must consider factors such as the maturity of the fund, the political and social contexts, and the level of economic development in assessing this guidance.

The importance of a comprehensive planning

The planning initiatives started early. In February 1974, the Ministry of Finance submitted a parliamentary report entitled “The role of petroleum activity in Norwegian society,” which explained how the country’s oil wealth should be used to develop the country, with the Government playing a central role in the entire value chain of the industry. In 1983, the Tempo Committee, a group of experts appointed by the Government, formally introduced a Norwegian SWF project to manage oil revenues and only spend the fund’s actual returns. In 1986, the Ministry of Finance published the “Norwegian Long-term Programme, 1986– 1989,” in which it advocated establishing the fund. It wasn’t until 1990 that Norway established the Government Petroleum Fund via a parliamentary act.

Norway did not establish its oil fund based on an impulse or misguided sociopolitical jockeying or to show off. There was a sequence of careful consideration and actions and key stakeholders’ involvement, including technocrats and academics working in close collaboration with politicians. The Government tasked experts with in-depth studies to ensure decisions were evidence-based.

Through planning, the Norwegian Government avoided haphazard actions, which often stem from a lack of evidence and strategic planning. The planning phase also provided a basis for the Government to anticipate and manage risks because it considered different scenarios which could emerge due to various domestic and external factors.

Development of a coherent investment strategy

The investment strategy of Norway’s Oil Fund, developed over time, is centered on investing in a diverse portfolio of foreign assets and businesses with a long- term focus. A cornerstone of the strategy is, therefore, a geographic focus on markets outside of Norway. The investments are also diversified across equities, bonds, real estate, renewable energy, and more. The Fund’s strategy is articulated in the management mandate of the Ministry of Finance.

The Fund has so far met its diversification target through its investments across 74 countries in 9,200 companies. In Africa, the Fund has investments in Morocco,Tunisia, Egypt, Ghana, Nigeria, Kenya, Tanzania, Botswana, and South Africa. It has a portfolio worth over USD 8 billion (as of February 2021) on the continent. The critical lesson isn’t that African SWFs should implement the same investment strategy as the Fund. Instead, the Norwegian experience illustrates the importance of establishing an investment strategy aligned with the overall mission of the SWF and the mechanisms available to achieve it. For the Fund’s managers, a diversified portfolio outside the country is consistent with its mandate. Finally, it is worth noting that the Fund’s investment strategy is not static. Norges Bank, the Central Bank of Norway, and the Fund Manager, regularly revisit it every three years with a comprehensive rationalization.

A robust governance structure

The Fund has effective operational management that includes checks and balances.

- The Parliament has legal oversight on the oil industry via the Government Pension Fund

- The Ministry of Finance is the custodian of the Government Pension Fund Act.

- The Ministry of Finance tasks Norges Bank to manage the Expressly, the Norges Bank Investment Management (NBIM), the asset management unit of the Bank, undertakes this task.

- The Leader Group at NBIM sets guidelines and delegates tasks and investment mandates within their delegated areas of responsibility.

This governance model ensures that no one person or entity is too powerful. Powers and responsibilities are separated to protect the integrity of the system. The concept of good governance and separation of powers is critical in Africa, where politicians’ interference in public affairs is recurrent.

Furthermore, there is an established track record of competent professionals across many sectors who work for the Fund. It consistently attracts top talents who have a proven experience from the private and public sectors and are held accountable for their commitments.

Transparency and accountability

Although the Fund did not initially directly engage with civil society stakeholders, it has been quite transparent since its inception. Today, it is among the most transparent SWFs in the world. While critics continue to demand more transparency (the Fund managers rightly protect some confidential information from the public and competitors, since the Fund is an active participant in the financial markets), the Fund consistently avails annual reports of its operations, interim reports, management reviews, voting guidelines, strategic plans, and a plethora of other information that indeed constitute a library of information for interested Norwegian citizens. It is even possible to track all the current investments of the Fund across its portfolio.

African SWFs should also seek to be more transparent. Most SWFs in Africa do not publish annual reports or release independent audits. Transparency has a cost. However, transparency is a choice that not only engenders trust and confidence and is also suitable for business. Therefore African SWFs must increasingly strive to be more transparent in annual reports to be held accountable.

Flexibility in adapting to changes

Although much planning went into the Fund’s design, the government and other stakeholders have remained flexible in its management and oversight. For example, the following changes were made during the past two decades:

- In 2000, some emerging markets were added to the Fund’s benchmark equity index.

- Corporate and securities bonds were added to the Fund’s benchmark fixed- income index in 2002.

- A decision was made to increase equity investments from 40% to 60% in 2007.

- Real estate was included in the Fund’s asset class in 2008.

- In 2017, the Fund made its first real estate investments in Asia.

Flexibility ensures that the Fund is adapted to current market changes and not fixated in time.

Above all, a strong political will

Some may argue that this is the most critical factor in the success of the Fund. While this may be up for debate, it is clear that Norway’s political leaders were cognizant of many countries’ misfortune that could not manage the wealth of their natural resources. They sought to avoid the same fate for their country.

For 30 years, the key stakeholders committed to the Fund’s sustainability despite multiple leadership changes.

Over the years, under different leaderships, the parliament has passed many reforms to self-regulate its oversight of the Fund to make it more sustainable. In 2001, for example, the parliament voted the budgetary rule into law, based on a guideline proposed by the Ministry of Finance. The rule capped at 4% the allocation of the Fund’s value to the government’s yearly fiscal budget. This demonstrated a political commitment towards the Fund’s vision because the legal framework ensured that its real value is preserved for future generations.

African political actors must increase their commitment to SWFs if they genuinely want to improve their people’s livelihoods and lay a foundation for future generations’ prosperity, learning from the Norwegian model.

The Key Takeaways for African SWFs

Sovereign Wealth Funds have become a fancy buzzword for many countries rich in natural resources. However, an analysis of Norway’s Oil Fund and other significant SWFs indicates that the amount of income a country earns from its natural resources does not necessarily reflect its SWF performance. Although Norway has gained immensely from its oil wealth, so have many African countries. Yet, they can still significantly develop their SWFs.

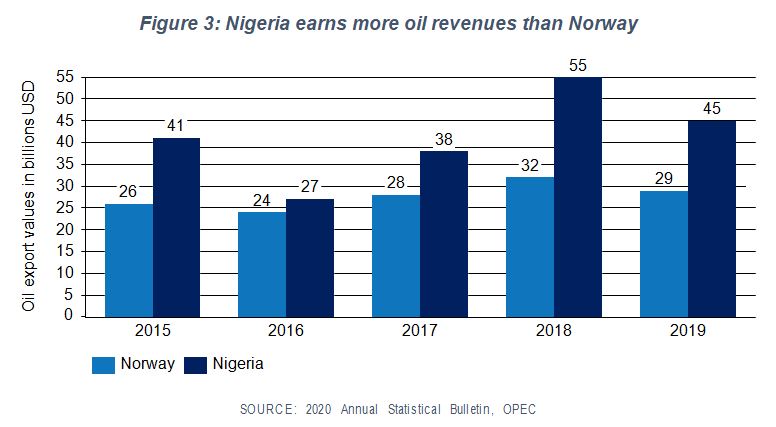

For example, Nigeria exported USD 206 billion worth of crude oil between 2015 to 2019 (OPEC). During the same period, Norway exported approximately USD 136 billion of crude oil. Considering that Nigeria began the commercial production of oil in 1958, it is easy to surmise the significant income the petroleum industry has brought to the country. Norway was not gaining as much in oil export income

when it created and developed its oil fund. As illustrated in the comparison below, that trend continues for revenue from oil from the two countries, from 2015 to 2019.

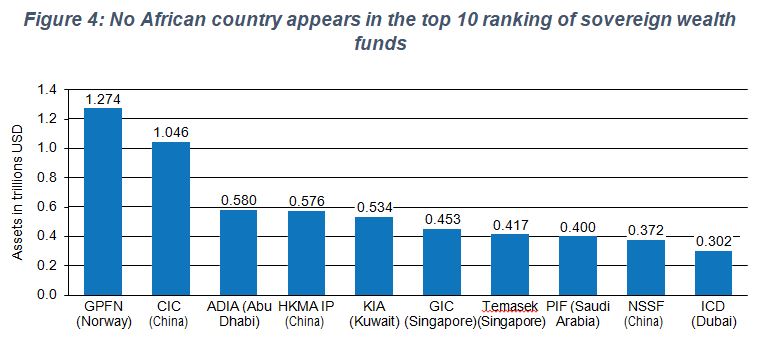

To illustrate this point further, it is essential to recall that not one African country figures on the top 20 largest SWFs globally, despite the significant inflow of revenues from natural resources. The elaboration and management of a successful SWF depend on other factors, of which the most fundamental is comprehensive planning. Will the Fund have a domestic investment focus or seek to invest in foreign markets? Is the country’s political will strong? How will the Fund be governed and managed? What mechanisms could allow the government to use the Fund to balance the fiscal budget sustainably? Who will manage the Fund, and how will they be held accountable? Will the Fund rely solely on revenues gained from a specific resource?

These are all questions that stakeholders must answer before establishing an impactful SWF, which would, in turn, help develop a coherent investment strategy that they could review periodically.

A strong management team could then successfully implement the investment strategy. However, management must be held accountable like in all great organizations. To achieve this, African SWFs should adopt Norway’s strategic choice to be transparent and open to changes within its Oil Fund. In other words, the general public should know the investments of their wealth fund and how well they are performing.

Finally, and perhaps most importantly, African leaders must have a formidable political will that stems from the love of one’s country and the personal satisfaction of having contributed to improving their people’s lives forever. It is a primordial agent of change that is needed to build effective SWFs in Africa.

SOURCE: Sovereign Wealth Fund Institute. Data as of April 20211.

With a SWF that is over three times the size of Saudi Arabia’s Public Investment Fund, Norway has demonstrated that any country could build a prosperous and sustainable economy for all its people. And achieving this would not be a miracle but merely a consequence of a strong political will, good planning, and timely execution of its mandate. This is the fundamental lesson from the sovereign wealth fund of Norway.

ABOUT THE AUTHOR

*Jeff Megayo is an Investment Officer in ACT Afrique’s Dakar offices. For comments on this article or to learn more about our NGO and Public Sector practice, email jmegayo@act- afrique.com.

1 GPFN is Norway Government Pension Fund Global; CIC is China Investment Corporation; ADIA is Abu Dhabi Investment Authority; HKMA IP is Hong Kong Monetary Authority Investment Portfolio; KIA is Kuwait Investment Authority; GIC is GIC Private Limited; Temasek is Temasek Holdings; PIF is Public Investment Fund; NSSF is National Council for Social Security Fund; ICD Investment Corporation of Dubai.